Table of Contents

Unpacking the Four Parts of Medicare and Their 2023 Costs

Part C: Medicare Advantage Plans

Part D: Prescription Drug Plan

Chiropractic Services Under Original Medicare

Cost Sharing for Chiropractic Care Under Medicare

Beyond Original Medicare: Considering Other Options

How Do I Know If Medicare Would Consider My Treatment “Medically Necessary”?

Understanding the scope of healthcare coverage can often be challenging, particularly when it comes to the intricacies of Medicare.

One common query is whether chiropractic services are covered under Original Medicare.

In short–yes, but it is very limited coverage that includes out of pocket expense.

This blog post aims to answer this question more in-depth and help you understand what costs may be associated with chiropractic services.

But first, let’s have a brief overview of the different parts of Medicare and what costs you should expect in general.

Unpacking the Four Parts of Medicare and Their 2023 Costs

Medicare, a federal health insurance program, is a crucial component of healthcare coverage for people aged 65 or older and younger individuals with certain disabilities.

This program is split into four parts: Part A, Part B, Part C, and Part D. Each part covers different services and comes with distinct costs.

Part A: Hospital Insurance

Medicare Part A, also known as Hospital Insurance, primarily covers inpatient care in hospitals. This includes critical access hospitals and inpatient rehabilitation facilities.

It also covers services like lab tests, surgeries, doctor visits, and home healthcare if you’re an inpatient in a hospital.

Furthermore, Part A provides coverage for skilled nursing facility (SNF) care. However, it’s important to note that this doesn’t include long-term care or custodial services.

Instead, it focuses on medically necessary care that can only be provided in an SNF, such as intravenous injections and physical therapy.

Part A also covers hospice care for people who are terminally ill and have a life expectancy of six months or less.

The coverage includes a variety of services such as medical, nursing, social services, drugs for symptom management and pain relief, physical and occupational therapy, and dietary counseling.

The costs associated with Part A can vary depending on the length of the hospital or SNF stay.

Most people don’t pay a monthly premium for Part A due to them or their spouse paying Medicare taxes while working.

Part B: Medical Insurance

Medicare Part B, also known as Medical Insurance, covers two types of services – medically necessary services and preventive services.

Part B covers things like durable medical equipment. Part B also covers many preventive services, including certain screenings, shots, and yearly “Wellness” visits to help prevent disease or detect it at an early stage when treatment is most likely to work best.

The standard monthly premium for Medicare Part B enrollees in 2023 is $164.90.

However, if your modified adjusted gross income reported on your IRS tax return from two years ago is above a certain amount, you may pay an Income Related Monthly Adjustment Amount (IRMAA) which is an extra charge added to your premium.

Part C: Medicare Advantage Plans

Medicare Part C, also known as Medicare Advantage Plans, are an alternative to Original Medicare (Parts A and B).

These plans are offered by private companies approved by Medicare and must offer at least the same benefits as Original Medicare but may do so with different rules, costs, and restrictions.

Due to high variation between benefits of different plans as well as variation by location, it may be helpful to speak with a licensed health insurance sales agent to help navigate the complexities of the options available to help find the plan that best fits your individual needs.

Part D: Prescription Drug Plan

Medicare Part D offers prescription drug plans to everyone with Medicare.

To get Part D, you need to join a plan run by an insurance company or other private company approved by Medicare.

The costs associated with Part D plans can vary widely based on the specific plan, the drugs you use, the pharmacy you choose, and whether you qualify for Extra Help from Medicare.

Each part of Medicare comes with its own set of covered services and associated costs which can change each year.

It’s important to stay updated and understand these costs to make informed decisions about your healthcare coverage.

You may also call 1-800-MEDICARE to speak with Medicare directly about your coverage eligibility and plan options available.

Chiropractic Services Under Original Medicare

Original Medicare does provide coverage for some chiropractic services. Specifically, Medicare Part B (Medical Insurance) covers manual manipulation of the spine if medically necessary to correct a subluxation.

However, there are several limitations to this coverage. For example, Medicare does not cover other services or tests ordered by a chiropractor, such as X-rays, massage therapy, and acupuncture.

In addition, Medicare doesn’t cover chiropractic treatments to extraspinal regions, which includes the head, upper and lower extremities, rib cage, and abdomen.

For a chiropractic service to be covered by Medicare, it must be considered medically necessary.

This means that the chiropractic care must be required to diagnose or treat an illness, injury, condition, disease, or its symptoms.

What Is a Subluxation?

Spinal subluxation is a term primarily used in the chiropractic field to describe a condition where one or more spinal vertebrae move out of position, causing an interruption in the normal functioning of the nervous system.

This misalignment can lead to a host of health issues. Various factors such as traumatic events, repetitive movements, poor posture, improper nutrition, stress, and exposure to toxins can cause subluxations.

The primary form of treatment for spinal subluxation is manual manipulation of the spine, a technique commonly associated with chiropractic care.

The aim is to reposition the misaligned vertebrae, restoring normal spinal mobility, reducing nerve irritability, and enhancing the patient’s overall health.

In cases of traumatic subluxations, particularly those affecting the cervical spine (the neck area), treatment options might include traction and open reduction. These cases are typically treated within a week.

Medicare and Medicaid coverage for the treatment of subluxation is limited to manual manipulation of the spine. However, it’s important to note that the necessity for treatment must be clearly established.

Manual manipulation of the spine is only covered for the treatment of spinal subluxations if it provides a therapeutic benefit to the patient.

In summary, spinal subluxation is a serious condition that requires prompt and appropriate treatment.

While spinal manipulation is the most common treatment approach, the specific treatment plan will depend on the severity and location of the subluxation, as well as the patient’s overall health.

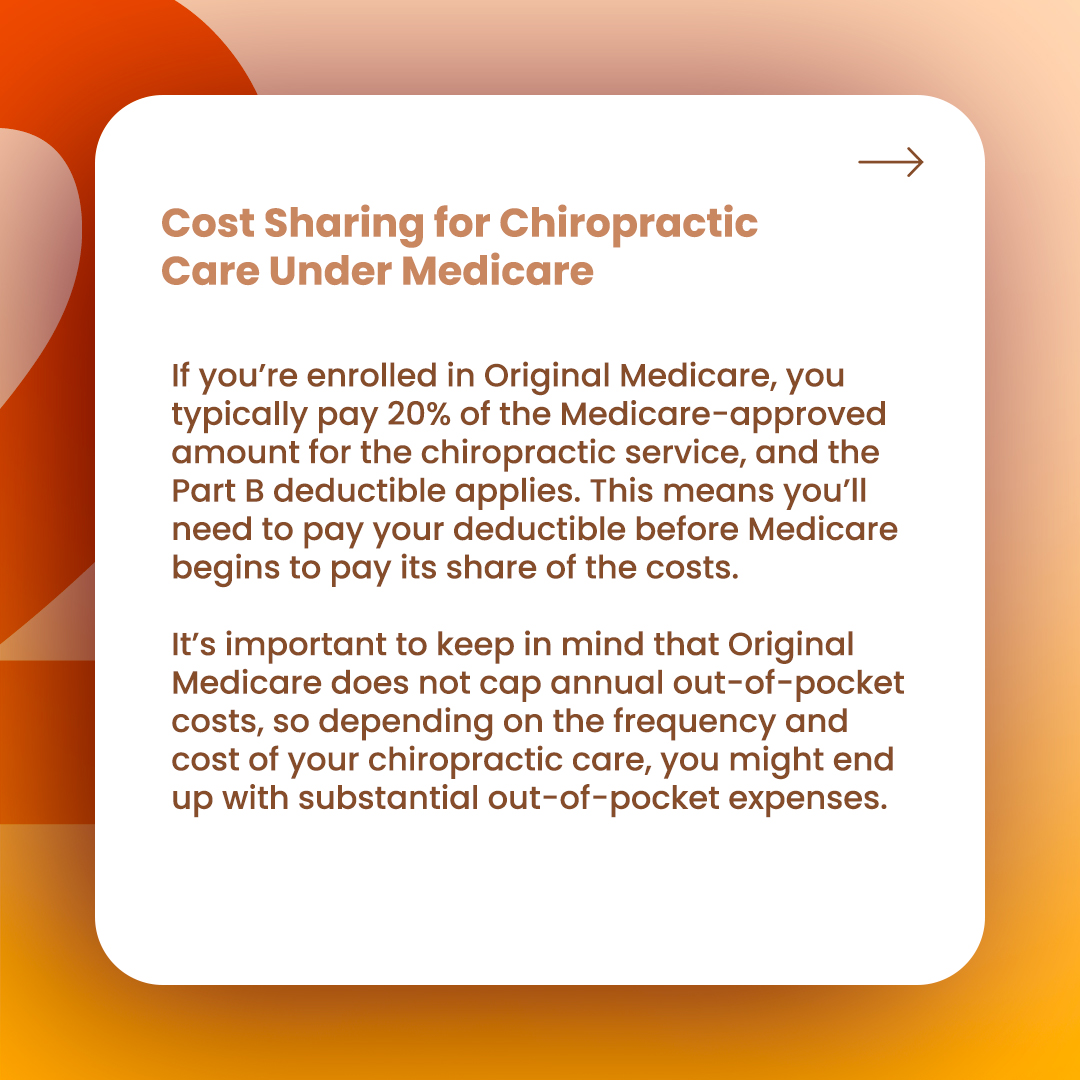

Cost Sharing for Chiropractic Care Under Medicare

If you’re enrolled in Original Medicare, you typically pay 20% of the Medicare-approved amount for the chiropractic service, and the Part B deductible applies.

This means you’ll need to pay your deductible before Medicare begins to pay its share of the costs.

It’s important to keep in mind that Original Medicare does not cap annual out-of-pocket costs, so depending on the frequency and cost of your chiropractic care, you might end up with substantial out-of-pocket expenses.

Beyond Original Medicare: Considering Other Options

While Original Medicare provides some coverage for chiropractic services, it’s limited.

If you require more comprehensive chiropractic care, you might want to explore alternatives.

Speaking with a licensed health insurance sales agent may help clarify what options may be available in your area that you are eligible for.

Medicare Supplement Insurance Plans, also known as Medigap, help pay some of the health care costs that Original Medicare doesn’t cover.

However, while Medicare Part B (Medical Insurance) covers manual manipulation of the spine if medically necessary to correct a subluxation when provided by a chiropractor or other qualified providers, Medigap policies generally do not cover additional services or tests ordered by a chiropractor, including X-rays, massage therapy, and acupuncture.

Therefore, it’s always advisable to check with your specific plan provider for detailed coverage information.

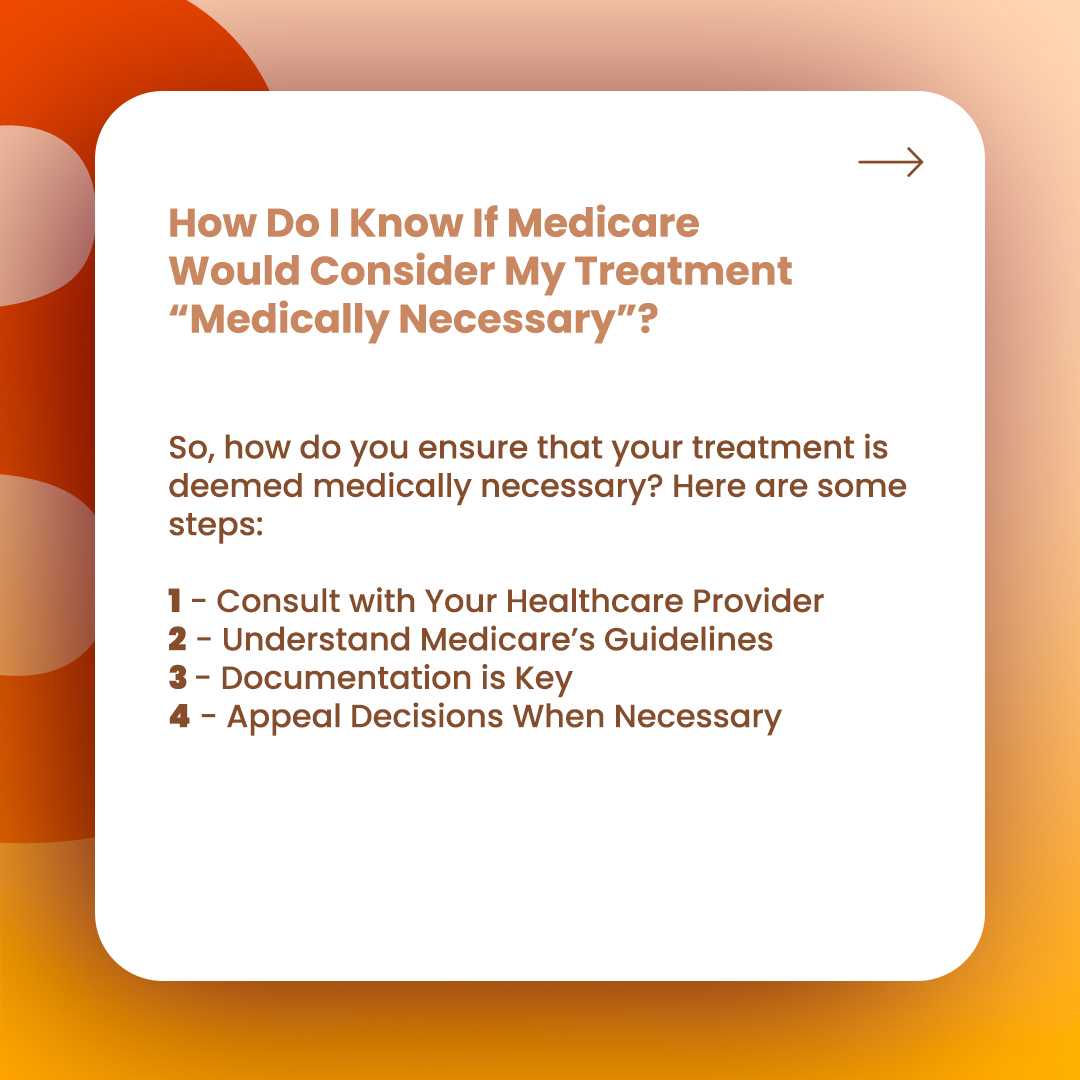

How Do I Know If Medicare Would Consider My Treatment “Medically Necessary”?

Navigating the healthcare landscape can be complicated, more so when it involves determining what Medicare deems as “medically necessary.”

Understanding this term and how to ensure your treatment is considered medically necessary is crucial to making the most of your Medicare benefits.

“Medically necessary” is a term used by Medicare to describe services or supplies needed to diagnose or treat an illness, injury, condition, disease, or its symptoms.

These services or supplies must meet accepted standards of medical practice. For Medicare to cover a specific treatment, it must fall under this definition.

So, how do you ensure that your treatment is deemed medically necessary? Here are some steps:

- Consult with Your Healthcare Provider: The first step is to have a detailed discussion with your healthcare provider about your health concerns.

They will assess your condition, consider your medical history, and recommend suitable treatments.

It’s essential to ask if the recommended treatment is considered medically necessary according to Medicare’s guidelines. - Understand Medicare’s Guidelines: Medicare has specific guidelines for different treatments and procedures.

These guidelines outline the conditions under which Medicare will cover a particular service or treatment.

You can find these guidelines on the official Medicare website or consult with a Medicare representative. - Documentation is Key: To prove a treatment’s medical necessity, proper documentation from your healthcare provider is crucial.

This documentation should include your diagnosis, why the treatment is necessary, and how the treatment will help improve your condition. - Appeal Decisions When Necessary: If Medicare denies your claim stating the treatment was not medically necessary, you have the right to appeal the decision. The denial letter will provide instructions on how to appeal.

In such cases, additional documentation from your healthcare provider explaining the medical necessity of the treatment could be beneficial.

Remember, just because a healthcare provider recommends a treatment does not automatically mean that Medicare will deem it medically necessary.

Always double-check with Medicare or your plan provider to avoid unexpected out-of-pocket costs.

To summarize, understanding Medicare’s definition of “medically necessary” and how to get your treatment categorized as such is fundamental to utilizing your Medicare benefits effectively.

Open communication with your healthcare provider, thorough knowledge of Medicare’s guidelines and proper documentation are all key in this process.

With careful planning and informed decisions, you can ensure you’re properly utilizing your healthcare coverage.

Please note that policies vary and the information might change, so it’s always a good idea to check with Medicare or your plan provider directly for the most accurate and up-to-date information.

In conclusion, Original Medicare does provide coverage for chiropractic care, but it is specifically limited to manual manipulation of the spine to correct a subluxation, if deemed medically necessary.

It’s important to remember that other services or tests ordered by a chiropractor, such as X-rays or massage therapy, are generally not covered.

As with all healthcare decisions, it’s crucial to understand the specifics of your coverage and consider your personal health needs when deciding on treatments.

Always consult with your healthcare provider about the best course of action for you. Medicare’s guidelines offer a base, but everyone’s healthcare journey is unique.

Stay informed, ask questions, and ensure you’re making the best decisions for your health.

-CALLING THE NUMBER ABOVE WILL DIRECT YOU TO A LICENSED INSURANCE AGENT.

By completing the form above, I understand that a Licensed Insurance Agent from Apollo Insurance Group may contact me via phone, email or mail to discuss Medicare insurance options. Calls may be made by auto dialer, text, or robocall and are for marketing purposes. Cellular carrier charges may apply. Providing permission does not impact eligibility to enroll or the provision of services. You can change permission preferences at any time by contacting (816) 608-4333. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options. Apollo Insurance Group is not affiliated with the federal Medicare program or the government. This is a solicitation for insurance.

I am a professional content writer specializing in the health insurance field. My work primarily focuses on simplifying the complexities of healthcare coverage, aiming to provide clarity and insight into an often confusing subject. Empowering people to make informed decisions about their well-being is my passion. At Apollo Health Insurance, we share that commitment. Apollo Health Insurance stands at the forefront of securing the best healthcare coverage for individuals, ensuring affordability without compromising on quality.

0 Comments