Table of Contents

Overview of the Parts of Medicare

Medicare Part A: Hospital Insurance

Medicare Part B: Medical Insurance

Medicare Part C: Medicare Advantage Plans

Medicare Part D: Prescription Drug Plans

What Out of Pocket Costs are Associated with Original Medicare?

Original Medicare and Routine Vision Care

Exceptions to the Rule: When Does Original Medicare Cover Vision Care?

Vision Coverage Comparison: Medicare Part B vs. Standalone Vision Plans

The Structure of a Standalone Vision Plan

What about Medicare Supplement Insurance Plans? Do they cover vision?

Healthcare, particularly vision care, is an essential aspect of our lives.

However, understanding the specifics of coverage, especially under large programs like Original Medicare, can be a daunting task.

This article aims to demystify the complexity surrounding vision coverage under Original Medicare and to provide clarity on the options available to beneficiaries.

Need Expert Help From A Licensed Medicare Agent?

Overview of the Parts of Medicare

Medicare is a federal health insurance program primarily designed for individuals aged 65 or older, although certain younger individuals with specific disabilities or illnesses may also qualify. Medicare is divided into four parts: Part A, Part B, Part C, and Part D, each covering different aspects of healthcare services.

Medicare Part A: Hospital Insurance

Medicare Part A, often referred to as hospital insurance, covers inpatient care provided in hospitals. It also includes coverage for skilled nursing facilities, hospice care, lab tests, and some home health care services. Most people do not have to pay a premium for Part A because they or their spouse paid Medicare taxes while working.

Eligible individuals who are 65 years old and above and have less than 40 quarters of coverage, as well as certain disabled individuals, have the option to voluntarily enroll in Medicare Part A by paying a monthly premium. Beneficiaries or their spouses who had at least 30 quarters of coverage or can choose to join Part A at a lower monthly premium rate. In 2023, the premium rate will increase by $4 to reach $278, compared to 2022.

Contact your local Social Security Agency or 1-800-MEDICARE for more information on your eligibility.

Medicare Part B: Medical Insurance

Medicare Part B is medical insurance that helps cover medically-necessary services like doctors’ services, outpatient care, home health services, and durable medical equipment. It also covers preventive services, such as clinical research and second opinions before surgery. Part B requires a monthly premium, which may vary depending on your income.

Medicare Part C: Medicare Advantage Plans

Medicare Part C, also known as Medicare Advantage, is an alternative to Original Medicare (Part A and Part B). These plans are offered by private companies approved by Medicare and include all benefits and services covered under Part A and Part B. Many Medicare Advantage Plans also include prescription drug coverage (Part D). The benefits of Medicare Advantage plans vary widely from plan to plan and by area. It may be useful or to speak with a licensed health insurance sales agent that may help you navigate the complexities of the options available to help ensure you find the coverage that best suits your needs.

Medicare Part D: Prescription Drug Plans

Medicare Part D Prescription Drug Plans offer prescription drug coverage to everyone with Medicare. To get Part D, you must join a plan run by an insurance company or other private company approved by Medicare. Each plan can vary in cost and specific drugs covered, and there may be late enrollment penalties associated with enrollment.

Medicare offers comprehensive health insurance coverage through its four parts, each designed to address different healthcare needs. Understanding these different parts and their coverage can help beneficiaries make informed decisions about their healthcare.

What Out of Pocket Costs are Associated with Original Medicare?

Original Medicare, which consists of Part A (hospital insurance) and Part B (medical insurance), involves several types of out-of-pocket costs. Here’s a breakdown:

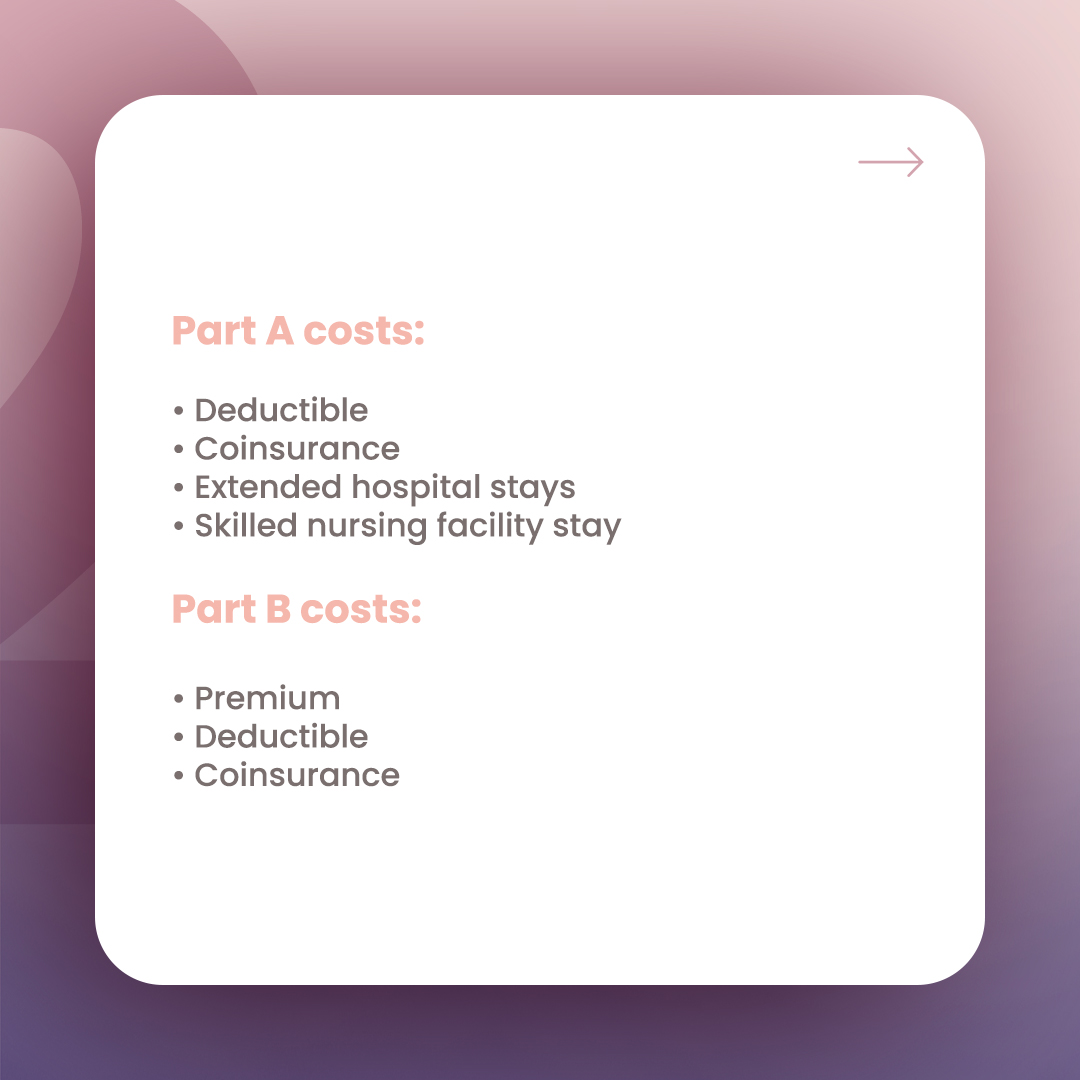

Part A costs:

- Deductible: For each benefit period in 2023, you pay a $1600 deductible before Medicare starts to pay its share.

- Coinsurance: If you’re in the hospital for more than 60 days in a benefit period, you pay a coinsurance amount per day. For days 61 through 90, it’s $400 per day in 2023.

- Extended hospital stays: For each “lifetime reserve day” used – these are additional days that Medicare will cover if you’re in a hospital for more than 90 days – you pay a coinsurance of $800 per day in 2023.

- Skilled nursing facility stay: You pay $200 coinsurance per day for days 21 through 100 in each benefit period for a skilled nursing facility stay.

Part B costs:

- Premium: The standard Part B premium amount in 2023 is $164.90. However, if your modified adjusted gross income as reported on your IRS tax return from 2 years ago is above a certain amount, you may pay an Income Related Monthly Adjustment Amount (IRMAA).

- Deductible: In 2023, you pay $226 for your Part B deductible.

- Coinsurance: After your deductible is met, you typically pay 20% of the Medicare-approved amount for most doctor services (including most doctor services while you’re a hospital inpatient), outpatient therapy, and durable medical equipment.

It’s important to note that these costs can change from year to year and you can inquire to Medicare directly about coverage by calling 1-800-MEDICARE.

Also, Original Medicare does not have a maximum limit on how much you can spend out-of-pocket in a year, which is different from many private insurance plans.

Original Medicare and Routine Vision Care

Original Medicare, comprising Part A (Hospital Insurance) and Part B (Medical Insurance), provides coverage for a range of healthcare services.

However, one area where coverage is limited is routine vision care.

Specifically, Original Medicare does not typically cover routine eye exams for eyeglasses or contact lenses. This means that beneficiaries are generally responsible for these costs out-of-pocket.

The absence of coverage for routine vision care may come as a surprise to some beneficiaries.

After all, regular eye exams are a critical part of maintaining overall health and wellness. They help detect vision problems early and can even aid in identifying other health issues, such as diabetes and high blood pressure.

Yet, despite their importance, these routine exams are not covered under Original Medicare.

Exceptions to the Rule: When Does Original Medicare Cover Vision Care?

While Original Medicare does not cover routine vision care, there are certain circumstances where vision coverage is provided.

One such circumstance involves individuals living with diabetes. For these individuals, Medicare Part B covers an annual eye exam for diabetic retinopathy.

Diabetic retinopathy is a common complication of diabetes that affects the eyes. If left undetected and untreated, it can lead to blindness. Therefore, the coverage of this annual exam by Medicare Part B plays a crucial role in early detection and treatment, helping to prevent severe vision loss.

Another exception to the rule involves beneficiaries who have undergone cataract surgery with an intraocular lens implant.

In these cases, Medicare Part B covers one pair of eyeglasses or contact lenses provided by a supplier enrolled in Medicare. This coverage is particularly important as it ensures beneficiaries have access to necessary vision correction following their surgery, aiding in their recovery process.

Vision Coverage Comparison: Medicare Part B vs. Standalone Vision Plans

Medicare Part B, part of the Original Medicare insurance program, provides limited coverage for vision care. This coverage does not extend to routine eye exams for prescribing, fitting, or changing eyeglasses or contact lenses.

Furthermore, most eyeglasses or contact lenses are not covered under Medicare Part B. However, Medicare Part B does cover some preventive and diagnostic eye exams, such as tests for glaucoma and macular degeneration. Beneficiaries with diabetes are entitled to an annual eye exam for diabetic retinopathy under Part B.

If you’ve undergone certain types of cataract surgery, Part B can also contribute towards the cost of corrective lenses.

On the other hand, standalone vision plans, which are separate from the Medicare program, typically offer more extensive coverage for vision care. These plans usually cover routine eye exams and corrective eyewear, such as glasses and contact lenses.

The specifics of what each plan covers can vary, so it’s crucial to review the details of each plan carefully. Standalone vision plans are often more comprehensive in their coverage compared to Medicare Part B. However, they also come with their own costs, and the benefits vary significantly from one plan to another.

In summary, while Medicare Part B offers limited vision coverage, mostly for preventive and diagnostic services, standalone

often provide broader coverage, including routine eye exams and corrective eyewear. It’s important for beneficiaries to understand these differences when considering their vision care needs.

By comparing the benefits and costs of Medicare Part B and standalone vision plans, beneficiaries can make informed decisions about which option best fits their individual needs.

The Structure of a Standalone Vision Plan

A standalone vision plan, distinct from general health insurance plans, is specifically designed to cover vision-related healthcare services.

While the specific structure of such plans can vary based on the provider and the plan itself, most standalone vision plans generally include the following components:

Premiums

Just like other types of insurance plans, standalone vision plans typically require the payment of a monthly premium. This is the amount you pay to the insurance company to keep your coverage active, regardless of whether you use the services or not.

Deductibles

Some vision plans may have a deductible, which is the amount you must pay out-of-pocket for your care before the insurance coverage kicks in. Not all vision plans have deductibles, and those that do might not apply them to all services.

Copayments and Coinsurance

After you meet your deductible (if there is one), you might be responsible for a copayment or coinsurance for each service. A copayment is a fixed amount you pay for a covered service, while coinsurance is a percentage of the cost of the service.

Covered Services

Standalone vision plans provide coverage for a range of vision-related services. These often include routine eye exams, eyeglass frames and lenses, contact lenses, and potentially even discounts on corrective eye surgeries like LASIK. The extent of coverage for these services varies by plan.

Network Restrictions

Many vision plans operate on a network basis, which means you’re required to see certain providers to get full coverage. Going out-of-network usually results in higher out-of-pocket costs.

Benefit Limits

There might be limits on how often you can receive certain services (like an annual eye exam) or how much the plan will pay for specific items (like a pair of glasses or contact lenses) within a certain timeframe, usually a year.

In summary, while the specific structure of standalone vision plans can vary, understanding these core components can help you make informed decisions about your vision care needs. Always remember to thoroughly review any plan you’re considering to ensure it aligns with your specific needs and budget.

What about Medicare Supplement Insurance Plans? Do they cover vision?

Medicare Supplement Insurance Plans, also known as Medigap, are designed to help cover some of the healthcare costs that Original Medicare (Part A and Part B) doesn’t cover, like coinsurance, copayments, and deductibles.

However, standard Medigap policies generally do not offer additional benefits for vision care, such as routine eye exams, eyeglasses, or contact lenses. These are considered “routine” services which are not covered by Original Medicare and thus not covered by Medigap either.

Always remember to review any insurance policy carefully to understand what is and isn’t covered before making a decision. And it may be helpful to talk with a licensed health insurance sales agent if you have questions on finding a plan that meets your needs.

As with any healthcare decision, it’s important for beneficiaries to thoroughly research their options and understand what each one entails. Consider factors such as cost, coverage, provider network, and other personal healthcare needs.

Remember, making informed decisions about your healthcare is a crucial step towards maintaining your overall health and wellness.

Get your questions answered with a free plan comparison by a licensed health insurance sales agent at Apollo Insurance Group with no obligation to enroll. Calling (913) 279-0077 will direct you to a licensed sales agent.

Sources:

- Medicare.gov – Eye Exams Routine

- Medicare.gov – Eye Exams for Diabetes

- Insurance.wa.gov – Does Medicare Cover Dental, Eye Exams or Hearing Aids?

- Medicare.gov – Eyeglasses & Contact Lenses

- Vision Coverage Comparison: Medicare Part B vs. Standalone Vision Plans

- Medicare.gov – Eye Exams Routine

- Medicare.gov – Eyeglasses & Contact Lenses

- SSA.gov – Plan for Medicare

- SSA.gov – How and when to apply for Medicare

- Medicare.gov – What’s Medicare

- Medicare.gov – What Medicare covers

- HHS.gov – What does Part B of Medicare (Medical Insurance) cover?

- Medicare.gov – Your Medicare coverage choices

- Medicare.gov – Part A costs

- Medicare.gov – Part B costs

-CALLING THE NUMBER ABOVE WILL DIRECT YOU TO A LICENSED INSURANCE AGENT.

By completing the form above, I understand that a Licensed Insurance Agent from Apollo Insurance Group may contact me via phone, email or mail to discuss Medicare insurance options. Calls may be made by auto dialer, text, or robocall and are for marketing purposes. Cellular carrier charges may apply. Providing permission does not impact eligibility to enroll or the provision of services. You can change permission preferences at any time by contacting (816) 608-4333. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options. Apollo Insurance Group is not affiliated with the federal Medicare program or the government. This is a solicitation for insurance.

I am a professional content writer specializing in the health insurance field. My work primarily focuses on simplifying the complexities of healthcare coverage, aiming to provide clarity and insight into an often confusing subject. Empowering people to make informed decisions about their well-being is my passion. At Apollo Health Insurance, we share that commitment. Apollo Health Insurance stands at the forefront of securing the best healthcare coverage for individuals, ensuring affordability without compromising on quality.

0 Comments