Critical illness insurance is often touted as a valuable financial safety net, offering protection in the event of serious health issues.

While this type of insurance can indeed be beneficial, it’s essential to be aware of its disadvantages before making a decision.

In this blog, we’ll explore some of the drawbacks associated with critical illness insurance, helping you make an informed choice about whether it’s right for you.

Contact Us For Fast & Easy Health Quotes

What is Critical Illness Insurance

Critical illness insurance is a type of insurance that pays a lump-sum cash benefit if you are diagnosed with a covered illness.

This money can be used for any purpose, such as paying for medical expenses, living expenses, or debt repayment.

Critical illness insurance is typically purchased as a supplement to health insurance. Health insurance can help cover the cost of medical care, but it may not cover all of the expenses associated with a critical illness.

Critical illness insurance can help cover these costs, as well as other expenses such as travel expenses for treatment or childcare costs while you are recovering.

Some of the most common critical illnesses covered by insurance include:

- Cancer

- Heart attack

- Stroke

- Major organ failure

- Coronary artery bypass surgery

- Multiple sclerosis

- Alzheimer’s disease

- Parkinson’s disease

- Muscular dystrophy

- Burns

- Blindness

- Paralysis

Critical illness insurance can be purchased from a variety of insurance companies, and policies can vary widely in terms of coverage, benefits, and cost.

Here are some of the benefits of having critical illness insurance:

- It can help you pay for medical expenses that are not covered by health insurance.

- It can help you cover living expenses while you are out of work or unable to work.

- It can help you pay off debt.

- It can give you peace of mind knowing that you will have financial support if you are diagnosed with a critical illness.

If you are considering purchasing critical illness insurance, it is important to talk to an insurance agent to learn more about your options and to choose a policy that is right for you.

How Does Critical Illness Insurance Work

Critical illness insurance works by paying you a lump-sum cash benefit if you are diagnosed with a covered illness.

This money can be used for any purpose, such as paying for medical expenses, living expenses, or debt repayment.

To purchase critical illness insurance, you will need to apply to an insurance company and be approved.

Once you are approved, you will need to pay a monthly premium.

The amount of the premium will depend on a number of factors, such as your age, health, and the amount of coverage you choose.

If you are diagnosed with a covered illness, you will need to file a claim with your insurance company.

The insurance company will review your claim and, if approved, will send you a lump-sum cash payment.

The amount of the payment will depend on the terms of your policy.

Most critical illness insurance policies cover a variety of illnesses, including cancer, heart attack, stroke, and major organ failure.

Some policies also cover conditions such as Alzheimer’s disease, Parkinson’s disease, and muscular dystrophy.

It is important to note that critical illness insurance is not a replacement for health insurance. Health insurance is still important for paying for the cost of medical care.

Critical illness insurance is designed to supplement health insurance and help you cover the other expenses associated with a critical illness.

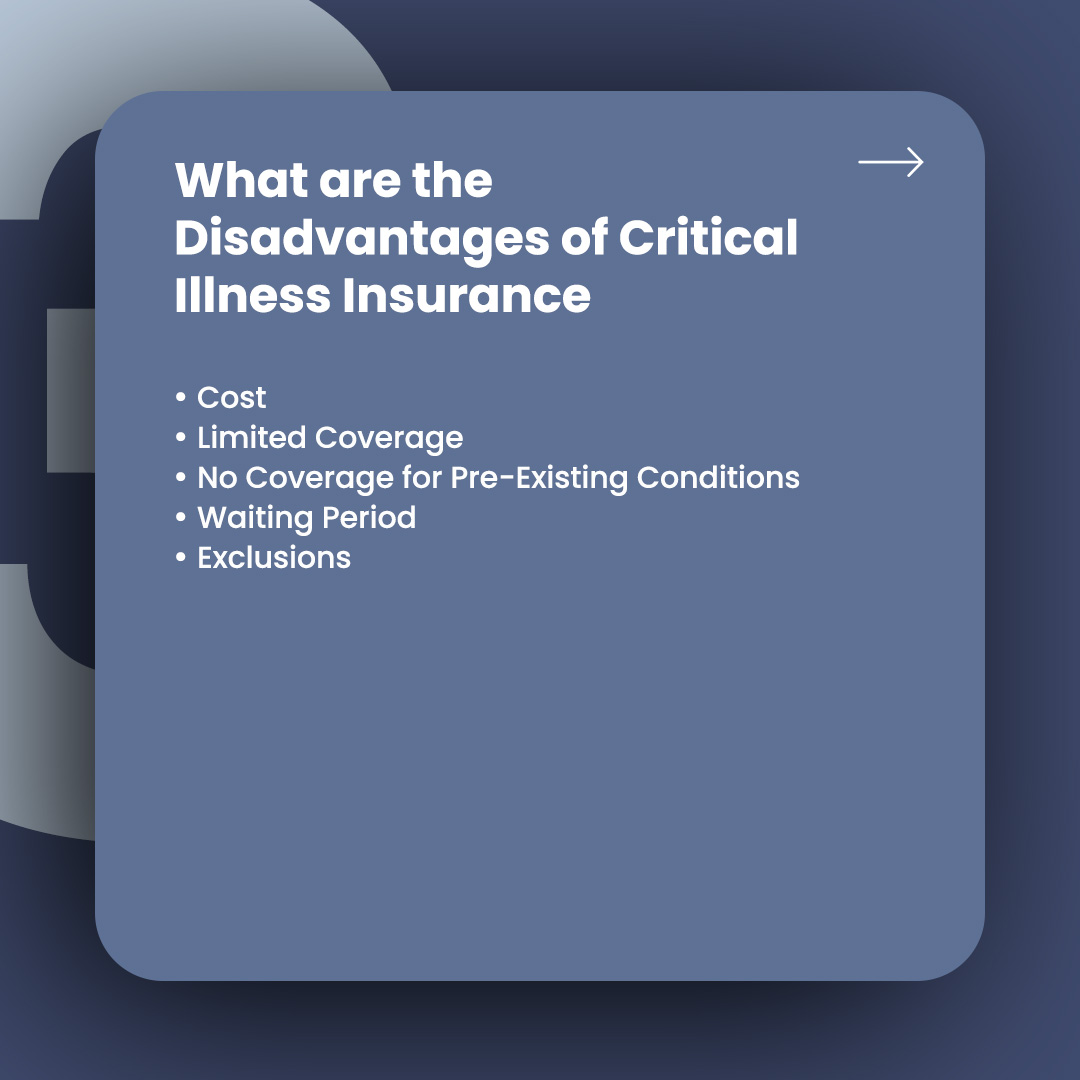

What are the Disadvantages of Critical Illness Insurance

While critical illness insurance can provide valuable financial protection in certain situations, it also comes with some disadvantages and limitations.

It’s important to consider these drawbacks when evaluating whether critical illness insurance is right for you:

-

Cost:

- Critical illness insurance can be expensive, especially for older individuals or those with pre-existing health conditions.

-

Limited coverage:

- Most critical illness insurance policies only cover a limited number of illnesses. It is important to read the policy carefully to understand what illnesses are covered and what exclusions apply.

-

No coverage for pre-existing conditions:

- Critical illness insurance policies typically do not cover pre-existing conditions. This means that if you have already been diagnosed with a critical illness, you will not be able to purchase critical illness insurance to cover that illness.

-

Waiting period:

- Most critical illness insurance policies have a waiting period before coverage begins. This means that you will have to wait a certain period of time after you purchase the policy before you can file a claim.

-

Exclusions:

- Critical illness insurance policies often have exclusions that apply to certain types of claims. For example, some policies may exclude claims related to suicide, drug abuse, or alcohol abuse.

It is important to weigh the pros and cons of critical illness insurance before you decide whether or not to purchase a policy. If you are considering purchasing critical illness insurance, be sure to compare different policies carefully and talk to an insurance agent to learn more about your options.

Here are some additional things to keep in mind about critical illness insurance:

-

Payout amounts may not be enough to cover all of your expenses:

- The payout amount on a critical illness insurance policy may not be enough to cover all of your expenses, such as medical bills, living expenses, and debt repayment. It is important to make sure that you have enough other financial resources in place to cover any shortfall.

-

You may not need critical illness insurance:

- If you have a good health history and adequate financial resources, you may not need critical illness insurance.

However, if you have a family history of critical illness or if you have a high-risk job, critical illness insurance may be a good option for you.

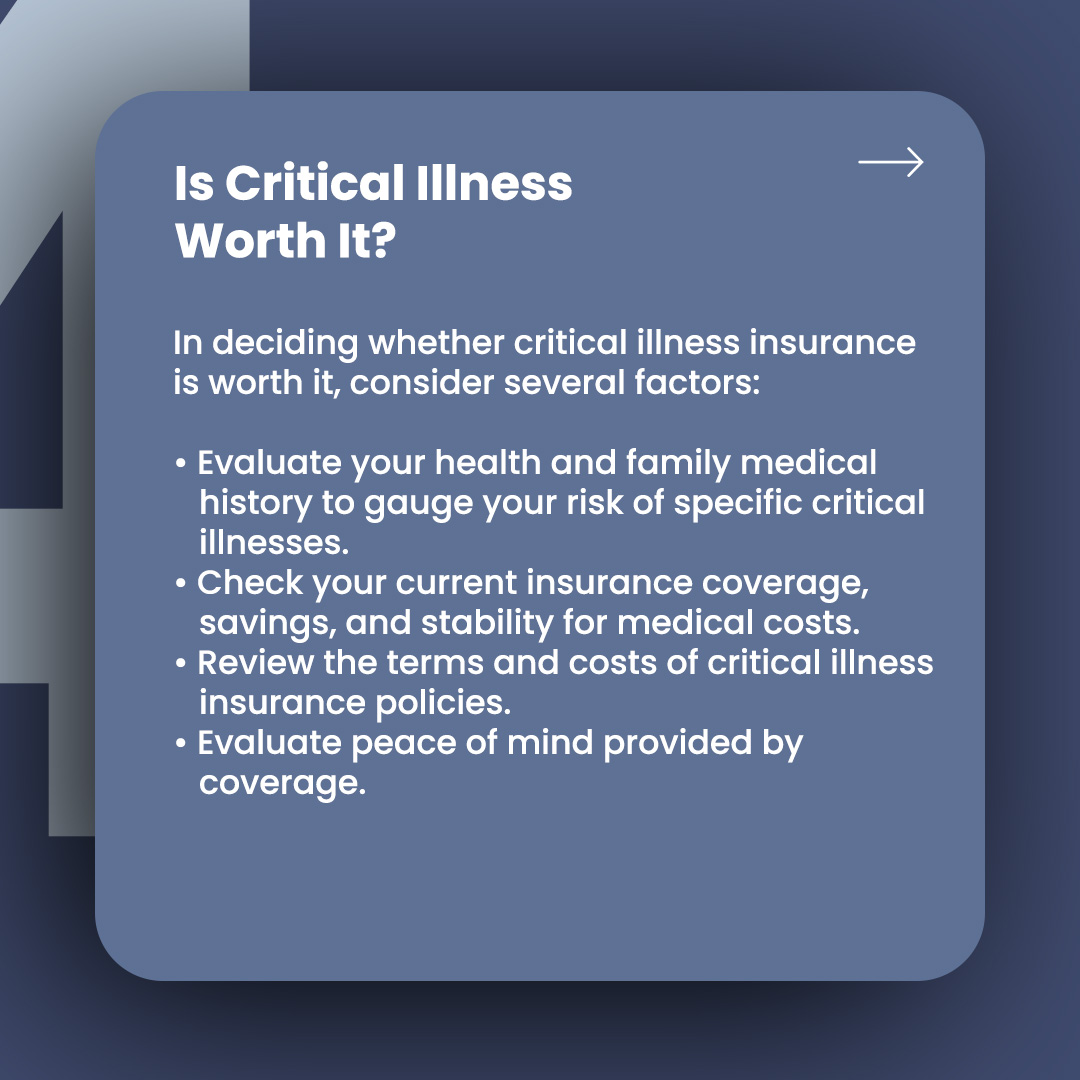

Is Critical Illness Insurance Worth It

In deciding whether critical illness insurance is worth it, consider several factors.

First, evaluate your health and family medical history to gauge your risk of specific critical illnesses. Additionally, assess your existing insurance coverage, emergency fund, and financial stability to determine if you can handle medical expenses without additional insurance.

Your lifestyle choices and risk factors, as well as the peace of mind provided by such coverage, should also be considered.

Next, carefully review the terms and costs of critical illness insurance policies, ensuring they align with your needs and budget.

Keep in mind that this insurance does not cover long-term care needs, which may require separate coverage.

Lastly, remember that the decision to purchase critical illness insurance is a personal one, influenced by individual preferences, risk tolerance, and financial goals.

Seeking advice from a financial advisor or insurance professional can help you make an informed choice based on your unique circumstances.

Critical illness insurance can provide valuable financial support during challenging times, but it’s essential to weigh its disadvantages against the benefits.

Before purchasing a policy, carefully consider your specific needs, financial situation, and the likelihood of developing a critical illness.

It’s also a good idea to consult with a financial advisor to determine if this type of insurance aligns with your overall financial goals and risk tolerance.

By being well-informed, you can make a decision that best suits your circumstances.