Table of Contents

What types of health insurance cover dermatology services?

How much does it cost to visit a dermatologist?

What factors deem someone eligible for coverage on dermatology visits?

What are some alternatives to using health insurance to pay for dermatology visits?

What questions should you ask your insurer before scheduling an appointment with a dermatologist

Do you have a health plan that covers dermatologist visits?

Are you looking for simple answers on what to expect from your insurance coverage when it comes to seeing a specialist in skin care and other related treatments?

There are many factors to consider, such as the specifics of your health plan and its policies for doctor visit reimbursement.

In this blog post, we will explore how different types of health plans handle dermatology services so that you can identify what to expect regarding coverage for physician consultations and procedures.

")

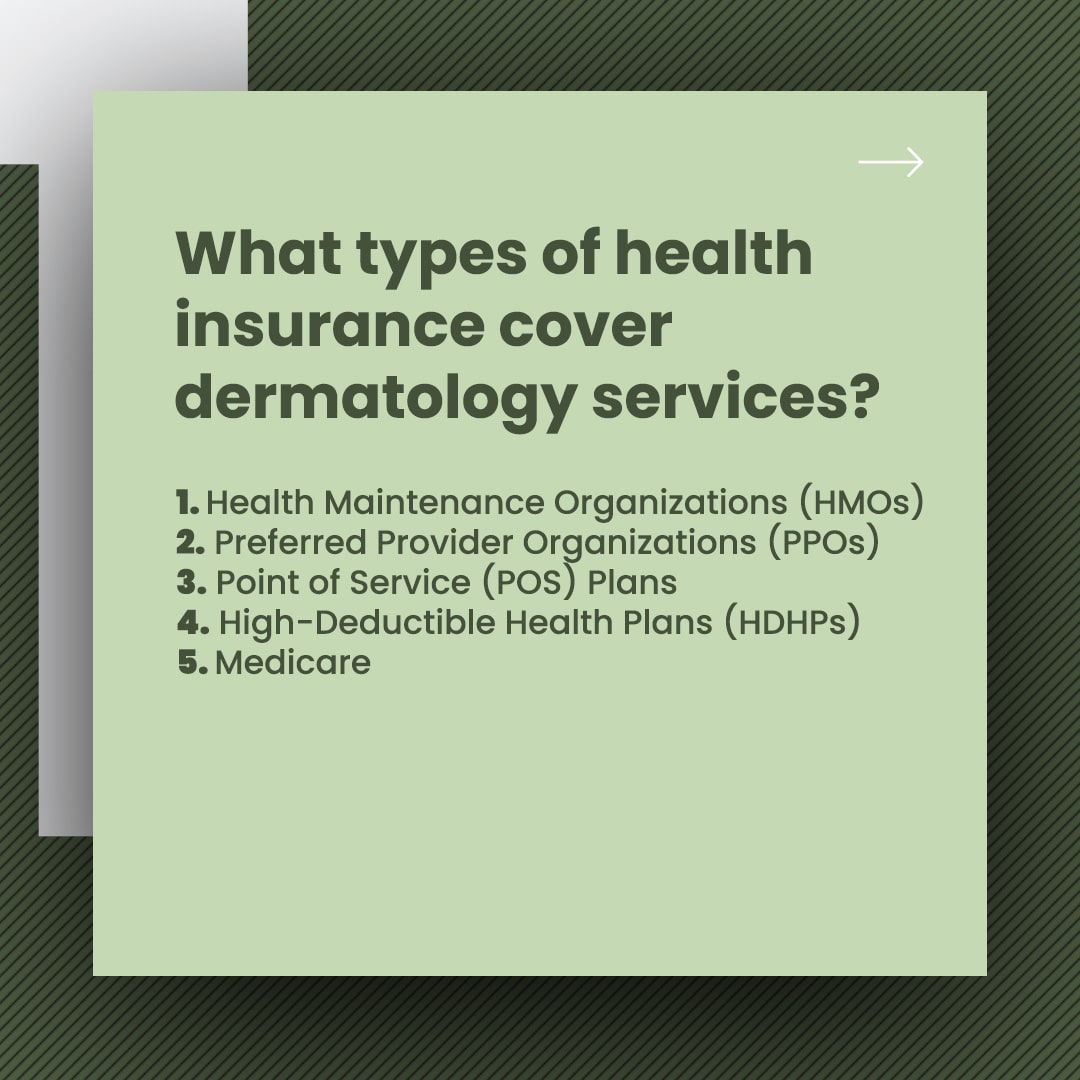

What types of health insurance cover dermatology services?

Taking care of our skin is important, and having health insurance that covers dermatology services plays a big part in that. Getting treatment for skin conditions can be expensive, so it pays to be aware of which health insurance plans offer coverage for dermatology services.

In this blog section, we’ll take a closer look at the types of health insurance that provide coverage for dermatology services, as well as what you need to know about deductibles, co-pays, and other expenses.

1. Health Maintenance Organizations (HMOs)

HMOs are a type of health insurance that typically offer the lowest out-of-pocket costs for dermatology services. However, they also tend to have the most restrictions when it comes to choosing your own healthcare provider. With an HMO, you typically have to choose a primary care physician who will refer you to a dermatologist if one is needed. If you go outside of your network, you may face additional costs.

2. Preferred Provider Organizations (PPOs)

PPOs are another type of health insurance that cover dermatology services. With a PPO, you can see a specialist without needing a referral from your primary care physician. However, you may still face higher out-of-pocket costs if you go out of network. PPOs tend to be more flexible than HMOs, but they also tend to have higher premiums.

3. Point of Service Plans (POS)

POS plans are a hybrid of HMOs and PPOs. With a POS plan, you’ll still need to choose a primary care physician, but you’ll also have the option of seeing specialists outside of your network. However, you may face higher costs if you go outside of the network. POS plans tend to offer more flexibility than HMOs but less than PPOs.

4. High-Deductible Health Plans (HDHPs)

HDHPs are a type of health insurance that have lower premiums but higher deductibles. With an HDHP, you’ll typically pay the full cost of dermatology services until you meet your deductible. However, once you meet your deductible, your insurance will cover the remaining costs. HDHPs are a good option if you’re generally healthy and don’t need to see a dermatologist often.

5. Medicare

If you’re age 65 or over, or have a disability, you may be eligible for Medicare. Medicare Part B may provide some coverage for dermatology treatments deemed medically necessary. The beneficiary will still be responsible for 20% copay as well as the part B deductible. Medicare will not cover cosmetic treatments. To help understand Medicare plan options that may help cover the 20% copay, it is a good idea to speak with a licensed insurance sales agent.

Having health insurance that covers dermatology services is important for maintaining your skin health. HMOs, PPOs, POS plans, and HDHPs all offer varying levels of coverage for dermatology services, so it’s important to choose the plan that best fits your needs and budget. If you’re over the age of 65 or have a disability, you may be eligible for Medicare, which also covers dermatology services.

Be sure to check with your insurance provider to understand your plan’s coverage and what expenses you may be responsible for.

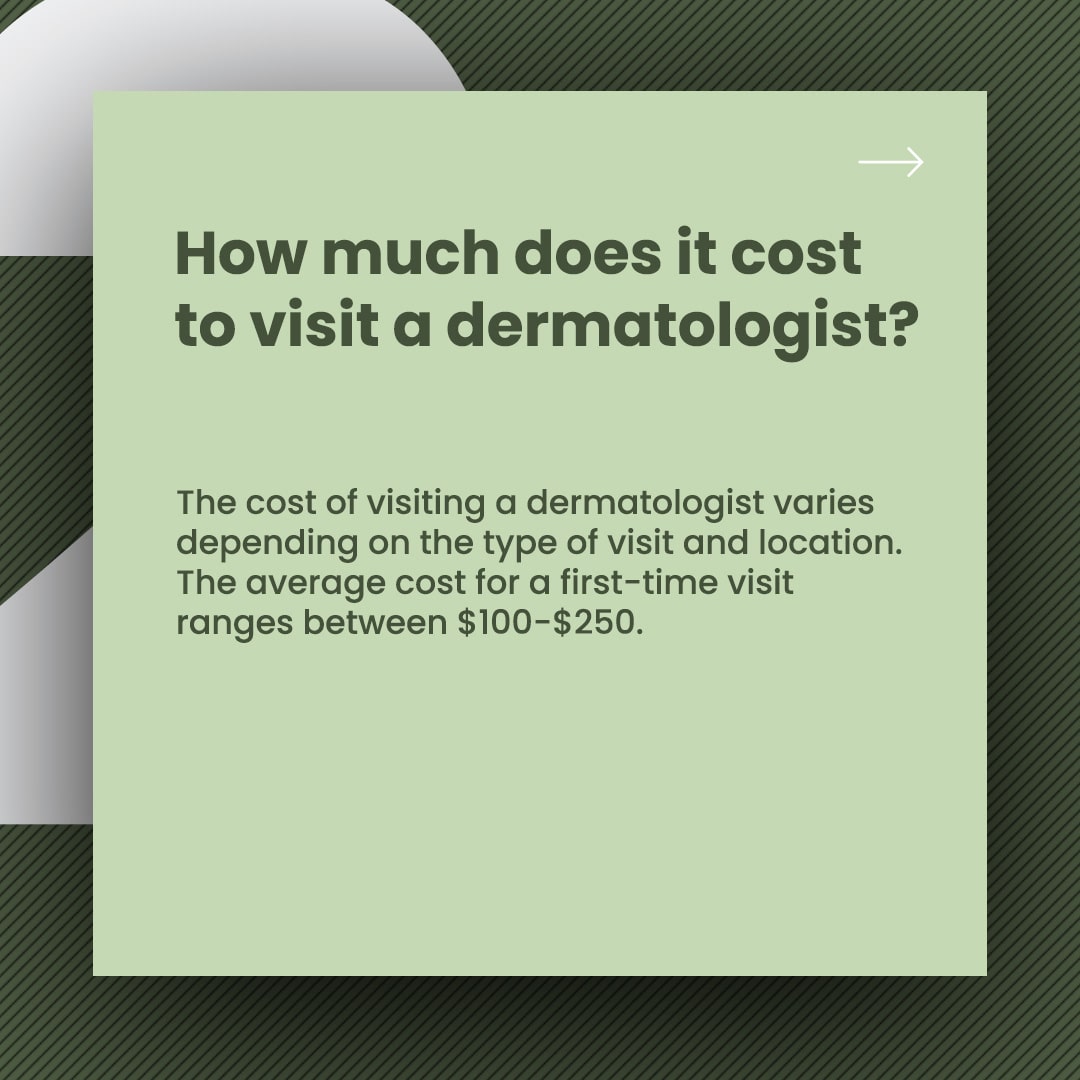

How much does it cost to visit a dermatologist?

The cost of visiting a dermatologist varies depending on the type of visit and location.

The average cost for a first-time visit ranges between $100-$250.

This initial visit may include a consultation and exam that assesses your skincare needs, followed by a personalized treatment plan and recommendations. Depending on the clinic and insurance coverage, additional costs may apply for lab tests, biopsies, or other treatments.

Factors impacting the cost of visiting a dermatologist include the location of the clinic, the type of procedure, and the level of experience of the dermatologist.

If you live in a metropolitan city, you may pay more for the same procedure than if you reside in a small town. Similarly, more complex treatments, such as Mohs surgery, will cost more than a routine check-up. Finally, dermatologists with more experience and certifications may charge more for their services.

Despite the initial costs, investing in our skin health may ultimately save us money in the long run. Taking care of our skin can prevent skin conditions from developing, cure existing issues, and even reduce the risk of skin cancer.

By identifying and treating skin problems early on, we can avoid costly, more invasive treatments down the line. Additionally, an investment in our skin health can increase our confidence and overall well-being.

For those without insurance, some dermatology clinics offer payment plans or sliding scales based on income.

If you have a flexible spending account (FSA), be sure to check if dermatology costs are eligible for reimbursement. Additionally, it is important to note that some insurance companies require a referral from a primary care provider before covering the costs of dermatology visits, so checking with your insurance provider is crucial.

In conclusion, visiting a dermatologist is an investment in our skin health and overall well-being. While the cost of visiting a dermatologist varies, factors such as location, type of procedure, and experience level of the dermatologist impact the price.

By identifying and treating skin problems early on, we can avoid costly, more invasive treatments down the line. For those without insurance, payment plans and sliding scales may be an option. Don’t let cost be a barrier to achieving healthy skin, schedule a visit with a trusted dermatologist today.

What factors deem someone eligible for coverage on dermatology visits?

Taking care of your skin is an essential part of overall health. Luckily, most insurance plans cover visits to the dermatologist for various skin concerns.

However, not all insurance plans include dermatology coverage, and even those that do may have specific eligibility requirements.

1. Health Insurance Plan

The first factor that determines eligibility for dermatology visits coverage is the type of health insurance plan you have. Most comprehensive insurance plans cover dermatology visits for medically necessary conditions.

However, this is not always the case, so you should check your policy documents or contact your provider to confirm coverage.

2. Reason for Visit

Not all visits to the dermatologist are covered by insurance. Typically, insurance plans will cover visits for a medical concern, such as skin cancer, psoriasis, or eczema. Cosmetic concerns like wrinkle treatment or laser hair removal may not be covered under most insurance plans, as they are typically considered elective procedures.

3. Referral and Authorization

Your insurance plan may require a referral from your primary care physician or authorization from the insurance company before seeing a dermatologist.

Check with your insurance provider to determine if this is necessary, and if so, make sure you have all the necessary paperwork and approvals in place before scheduling an appointment.

4. Copayments and Deductibles

Like most medical visits, you may be required to pay a copayment or meet a deductible before insurance coverage begins. Copayments and deductibles vary depending on your insurance plan, so be sure to double-check your specific plan’s terms beforehand.

5. Out of Network Services

Health insurance networks can vary and the provider you choose may be out of network. If that is the case, coverage for your dermatology visits may be limited, or you may be required to pay out of pocket.

Make sure you confirm which dermatologists are in your network or look for an in-network provider near you.

Overall, it’s important to be aware of your eligibility for dermatology visit coverage. Checking with your insurance provider, confirming required referrals/authorizations, and being prepared to take care of any copayments or deductibles will help ensure you are using your insurance most effectively.

By understanding the requirements, you can maximize your coverage for dermatology visits.

Remember, taking care of your skin is vital to your overall health, so make sure you make it a priority.

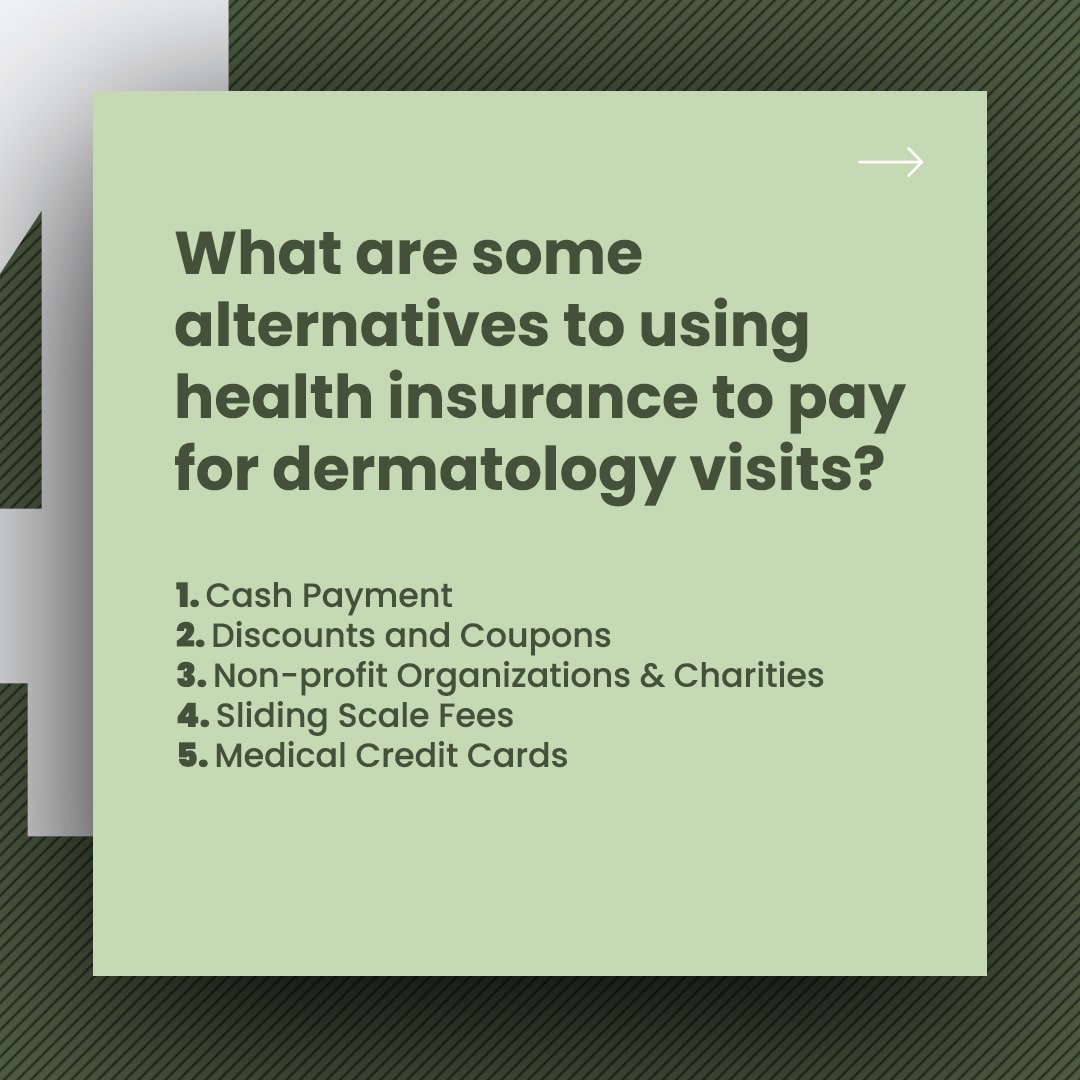

What are some alternatives to using health insurance to pay for dermatology visits?

1. Cash Payment

Believe it or not, many dermatologists still accept cash payments. Paying with cash means that you’ll have to negotiate the price ahead of time, leaving out any excess charges that come with paying with insurance.

It’s always worth asking if cash payments may be an option for your dermatology needs.

2. Discounts and Coupons

Another option for saving on payments for dermatology visits is to look for discounts or coupons. Dermatologists often offer promotions like “first-time customer discount” or “15% off your first visit”.

You can also save money by booking appointments during off-peak hours, or accepting a consultation with a resident dermatologist who is still learning the ropes but is still a licensed professional.

3. Non-profit Organizations & Charities

Many non-profit organizations and charities offer free clinics that provide dermatology services. These types of organizations often have a volunteer medical staff, so it might take longer to get an appointment at these clinics. However, they’re still a useful resource for people who have no access to health insurance.

4. Sliding Scale Fees

Some dermatologists offer their services on a sliding scale fee. This means their payment is based on your financial situation. In other words, you’ll only have to pay what you can afford based on your income. To find a dermatologist that offers sliding scales, do some research online, or reach out to community health centers.

5. Medical Credit Cards

Medical credit cards are a special type of credit card that covers medical expenses. They offer special terms and interest rates that make paying for medical treatments much easier. Some popular medical credit cards that cover dermatology visits include CareCredit, Flexcare Medical Staff Card, and Refund Advantage.

There are many alternatives to health insurance, which can help make dermatology visits more affordable. From cash payments to medical credit cards, there are options available to everyone.

If you’re still struggling to find alternatives to health insurance, try contacting community health centers, non-profit organizations, and charities. They might have resources available that can help you pay for your medical expenses. Remember, taking care of your health should be a top priority.

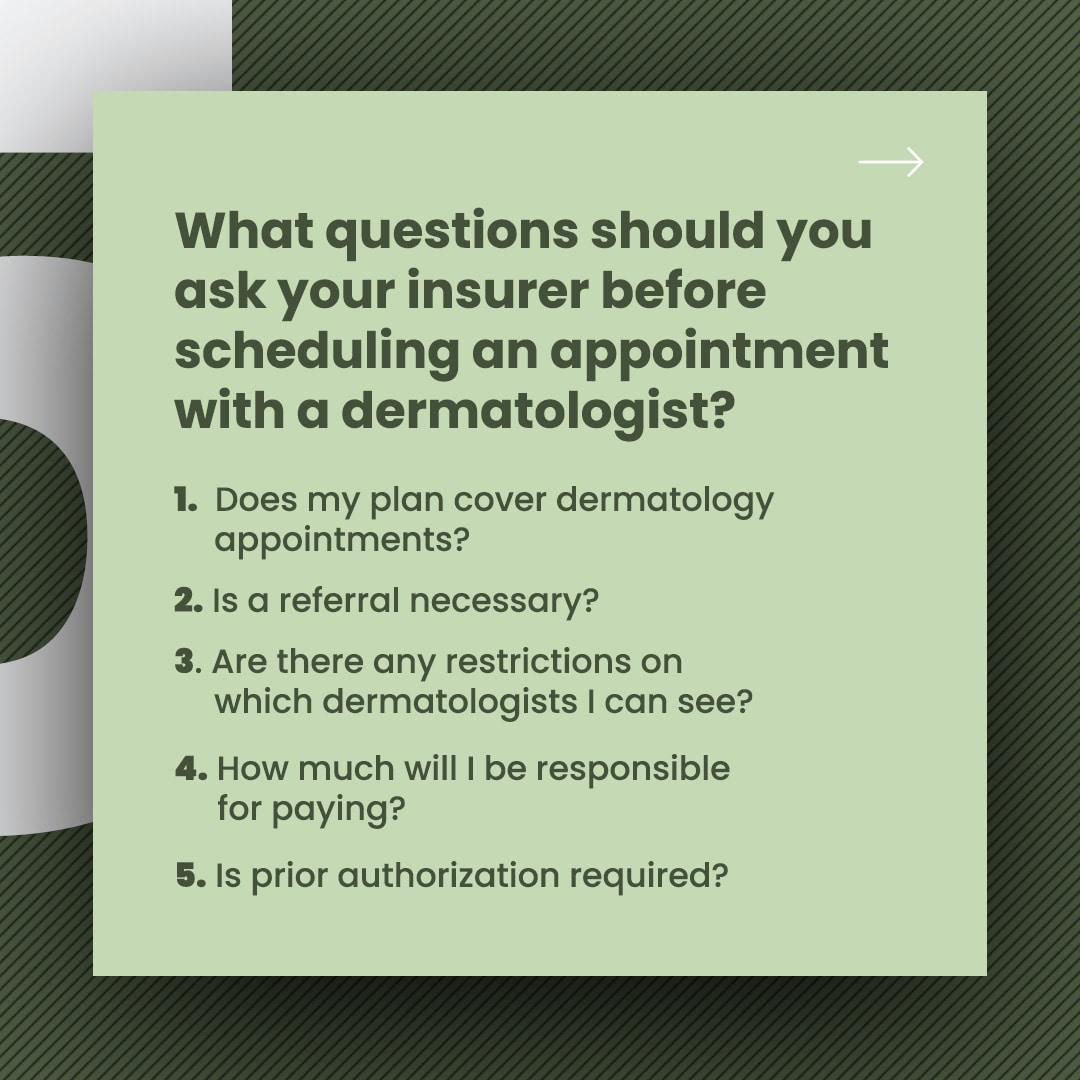

What Questions Should You Ask Your Insurer Before Scheduling an Appointment with a Dermatologist

Taking care of your skin is important, and sometimes that means scheduling an appointment with a dermatologist.

However, before you make that appointment, it’s important to confirm that your insurance provider will cover the cost. Insurance plans can vary greatly in terms of coverage and cost-sharing, and you don’t want to be hit with a surprise bill after your appointment.

Here are five questions to ask your insurance provider before scheduling a dermatology appointment.

1. Does my plan cover dermatology appointments?

The first question you should ask your insurance provider is whether or not your plan actually covers dermatology appointments. If you have health insurance through your employer, the coverage details should be outlined in your benefits package.

If you purchased insurance through the Health Insurance Marketplace, you should be able to find information about dermatology coverage on the plan’s website. If you’re not sure which type of plan you have or having difficulty finding information, don’t hesitate to call your insurer directly.

2. Is a referral necessary?

Some insurance plans require patients to get a referral from their primary care physician before seeing a dermatologist. If your plan does require a referral, make sure to get one before scheduling your appointment to avoid any issues with coverage.

3. Are there any restrictions on which dermatologists I can see?

Some insurance plans may have a network of preferred providers that you must see in order to receive coverage for your appointment. If you decide to see a dermatologist outside of your network, you may be responsible for a larger portion of the costs.

Additionally, some plans may require you to see a specific dermatologist within their network in order to receive coverage. Make sure you know the guidelines for your plan before scheduling your appointment.

4. How much will I be responsible for paying?

It’s common for insurance plans to have co-payments, co-insurance, and deductibles that patients are responsible for paying. Make sure you understand your plan’s cost-sharing requirements so that you’re not caught off guard by unexpected bills after your appointment.

If the cost of the appointment is a concern, you may want to consider reaching out to your dermatologist’s office to see if they offer payment plans or discounts for self-pay patients.

5. Is prior authorization required?

Finally, some insurance providers may require patients or their dermatologists to obtain prior authorization before the appointment can take place. This means that the dermatologist must provide the insurer with information about the patient’s medical history and the necessity of the appointment before the insurer will approve coverage.

This process can take several days, so make sure to factor in this extra time when scheduling your appointment.

Scheduling a dermatology appointment may seem like a straightforward process, but it’s important to confirm that your insurance provider will cover the costs beforehand. By asking these five questions, you can save yourself the headache of surprise bills and ensure that your appointment goes as smoothly as possible.

Remember, if you have any questions about your insurance coverage or the process of scheduling a dermatology appointment, don’t hesitate to reach out to your insurer directly.

In conclusion, health insurance typically covers visits to dermatologists for medical reasons. However, coverage may vary depending on the type of insurance plan and the specific treatment being sought. It’s important to check with your insurance provider to understand what is covered under your policy, such as copays, deductibles, and out-of-pocket expenses.

Additionally, some cosmetic dermatology procedures may not be covered by insurance.

Nevertheless, seeing a dermatologist for both medical and cosmetic concerns can help maintain the health and appearance of your skin.

For help on getting health insurance or if you have any questions, please reach out to a licensed sales agent!

Sources:

“Basics of Medicare Parts A,B,C and D.” North Carolina Dept. of Insurance. https://www.ncdoi.gov/consumers/medicare-and-seniors-health-insurance-information-program-shiip/basics-medicare-parts-b-c-d

“What’s Not Covered by Part A and Part B?” https://www.medicare.gov/what-medicare-covers/whats-not-covered-by-part-a-part-b

I am a professional content writer specializing in the health insurance field. My work primarily focuses on simplifying the complexities of healthcare coverage, aiming to provide clarity and insight into an often confusing subject. Empowering people to make informed decisions about their well-being is my passion. At Apollo Health Insurance, we share that commitment. Apollo Health Insurance stands at the forefront of securing the best healthcare coverage for individuals, ensuring affordability without compromising on quality.